What Is Fire Insurance?

Fire Insurance is a type of property insurance that covers losses or damages caused by fire. It is possible to cover the repair, replacement, or reconstruction costs of property as specified in the policy by purchasing this insurance policy.

What Is The Importance Of Fire Insurance?

Listed below are some of the reasons why you should purchase Fire Insurance and why it is a wise investment.

1. Loss or damage caused by any movable or immovable object that explodes in fire.

2. Fire Insurance covers things like furniture, office buildings, machinery, stock, and other property damage caused by a fire.

3. A burglary insurance policy also covers damages caused by natural calamities, explosions, bursting of water tanks, etc., in addition to fire-related perils.

Types of Fire Insurance Policies

- Bharat Sookshma Udyam Suraksha: Covers businesses with total insured property values up to ₹5 Crores. Ideal for small enterprises and startups.

- Bharat Laghu Udyam Suraksha: Suitable for medium-sized businesses, covering property with insured values between ₹5 Crores and ₹50 Crores.

- Standard Fire and Special Perils Policy (SFSP): Designed for larger businesses or corporates, covering property exceeding ₹50 Crores.

Fire Insurance Policies Based on Asset Type

Fire insurance policies also differ based on whether they cover fixed or non-fixed assets.

Fire Insurance Policies for Fixed Assets

Fixed assets typically include buildings, machinery, and permanent installations:

- Replacement Value Policy: Provides coverage equivalent to the current cost of replacing the damaged property with a new asset, accounting for depreciation.

- Reinstatement Value Policy: Covers the cost of restoring or reconstructing the property to its original condition before the fire occurred, without depreciation.

Fire Insurance Policies for Non-Fixed Assets

These assets include stock, inventory, goods in transit, and other movable items:

- Floater Policy: Ideal for insuring movable goods spread across multiple locations under one policy.

- Specific Policy: Covers assets for a specific amount, usually less than their total value, without penalisation for under-insurance.

- Comprehensive Policy: Offers broad protection against multiple risks, suitable for diverse business needs.

- Valued Policy: Insures assets at a pre-agreed value determined at the time of policy purchase, irrespective of market fluctuations.

- Valuable Policy: Covers assets based on their current market value at the time of loss or damage.

- Consequential Loss Policy: Covers financial losses resulting from business disruption due to a fire incident.

Fire Insurance Characteristics

There are certain characteristics associated with Fire Insurance Policies that make them unique from others. The following characteristics should not be overlooked:

Policy for a year: A term Fire Insurance Policy normally lasts for a year, but it can be renewed depending on its terms and conditions.

Insurable interest: When the insured owns an insurable interest in the insured property, the policy is valid. In the event of a loss, such interest may be required. In an insured’s favor, this ensures that the insured property survives, but in the event of a loss, the insured may have to suffer a loss as well.

Direct Loss: An individual may avail of this service if the loss or damage was caused by fire.

Personal right: A person whose name appears on the policy document will receive the insured amount in case of any loss/damage under any unfortunate circumstances.

Transparency: The policy requires complete transparency. The insured must understand the insured’s behavior. Also, the insured can only transfer the policy with the consent of the insurer only, and the insurer can terminate the policy if their possession of goods is transferred to a third party.

Property Description: When purchasing a Fire Insurance Policy, you should provide a detailed account of the possessions. In the event an unfortunate event occurs at the insured place, the claims will be settled according to the location outlined in the policy document. It is important to inform the insurer if there are any changes to avoid further repercussions.

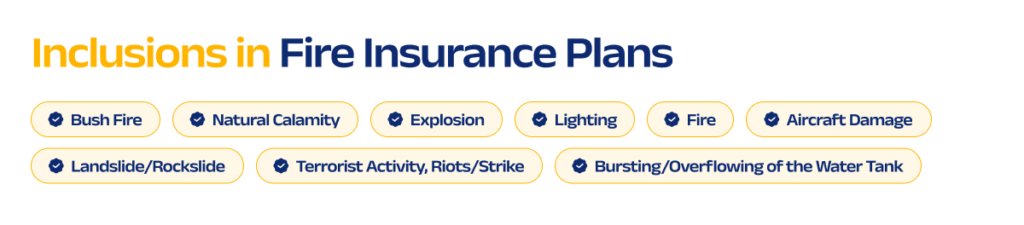

Inclusions in Fire Insurance Plans

| Fire | There is coverage for damage caused by fire, but not damage caused by natural heating, fermentation, or unconstrained burning. |

| Lighting | The insurance company will cover any damage/loss caused by lighting, for example, cracks in the roof or building. |

| Explosion | Under this policy, damage caused by a fire explosion is covered. |

| Aircraft Damage | The policy will cover damage caused by an aircraft, for instance, articles dropped by an aircraft, airborne devices, etc. |

| Terrorist Activity, Riots/Strike | Fire insurance covers any damage caused by a strike, riot, or any fear-mongering activity. |

| Natural Calamity | A policy covers all damages caused by storms, typhoons, and other natural calamities. |

| Landslide/Rockslide | Rockslides/landslides will cause destruction to your property. |

| Bursting/Overflowing of the Water Tank | In the event of a water tank burst or overflow, the insurance will cover the damage. |

| Bush Fire | The policy will cover the damage caused by setting fire to overgrown plants or shrubs. However, the policy will not cover the destruction caused by forest fires. |

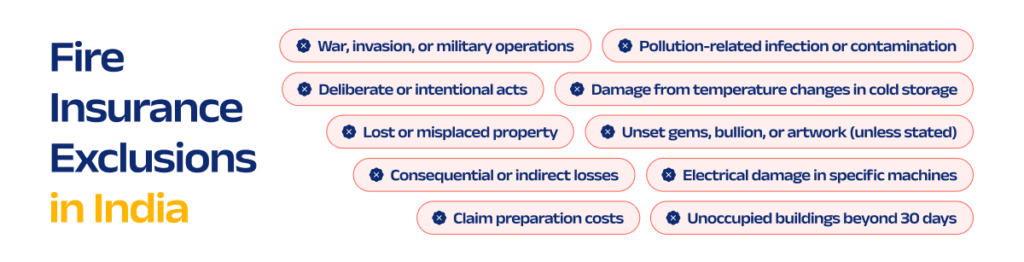

Fire Insurance Exclusions in India:

The following events are not covered by Fire Insurance:

1. An act that is deliberate, wilful, or intentional

2. Changes in temperature can damage or lose stocks in cold storage

3. Invasion, war, and military operations of a similar nature

4. Infection or contamination by pollution

5. Property that has gone missing or has been misplaced

6. Losses or damages resulting from consequential or indirect causes

7. The cost of preparing any claim, including fees and expenses

8. Unoccupied premises or buildings for more than 30 days are not insured.

9. A precious stone, bullion, or artwork that has not been set, unless otherwise stated

10.Electrical machines, short circuits, apparatus, leakage of electricity, etc. This exclusion applies to specific machines.

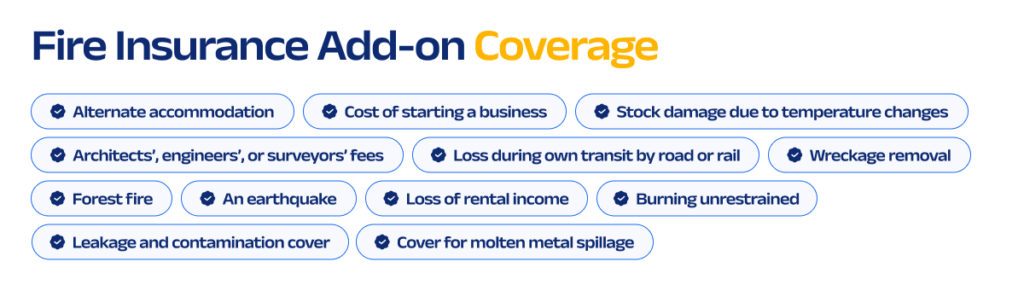

Fire Insurance Add-on Coverage

By paying an additional premium, the insured can receive the following additional coverage:

- An earthquake

- Wreckage removal

- Forest fire

- Loss of rental income

- Cost of starting a business

- Alternate accommodation

- Burning unrestrained

- Stock damage caused by temperature changes

- Leakage and contamination cover

- Fees for consultations with architects, engineers, and surveyors

- Cover for molten metal spillage

- Loss resulting from insured’s own transit by road or rail

Fire Insurance: Determining the Amount to be Insured

Selecting the appropriate sum insured is crucial to ensure adequate coverage. Consider the following methods:

- Reinstatement Value: Covers the cost of replacing the damaged property with a new one of similar kind without depreciation.

- Market Value: Considers the current value of the property after accounting for depreciation.

- Agreed Value: A pre-determined value agreed upon by both insurer and insured at the policy’s inception.

Who Should Buy Fire Insurance Policies in India?

Fire insurance is crucial for a wide range of businesses in India. Key businesses that should consider purchasing fire insurance include:

- Manufacturers and Industrial Units: Protects machinery, raw materials, and finished goods.

- Retailers and Wholesalers: Covers stock, inventory, and shop premises.

- Warehouses and Logistics Firms: Provides coverage for goods stored or in transit.

- Hospitality Businesses: Essential for hotels, restaurants, and entertainment venues to safeguard property and equipment.

- Commercial Office Spaces: Protects office equipment, documents, and fixtures.

- Educational Institutions: Covers infrastructure, laboratory equipment, and other essential educational assets.

Businesses of any size—small, medium, or large—can significantly benefit from fire insurance, ensuring their financial stability and continuity in case of unforeseen fire incidents.

Documents Required To File Fire Insurance Claim

When filing a fire insurance claim in India, it’s essential to provide the following documents:

- Insurance Policy Document: A certified copy of the policy, including all schedules and endorsements.

- Claim Form: Duly filled and signed, detailing the incident and estimated losses.

- Fire Brigade Report: Official documentation confirming the fire incident.

- First Information Report (FIR): Filed with the police, especially if foul play is suspected.

- Photographic Evidence: Photographs or videos showcasing the damage.

- Forensic Report: If applicable, to determine the fire’s cause.

- Inventory of Damaged Items: Detailed list with estimated values.

- Repair Estimates: Quotations from contractors for repair or replacement.

- Financial Records: To substantiate claims related to business interruption or loss of income.

Ensuring the accuracy and completeness of these documents can expedite the claim settlement process.

Frequently Asked Questions

1. How does impact damage occur?

A collision or impact damage occurs when an external object damages your insured property, like a car, bike, tree, etc.

2. Can you explain what reinstatement value is?

The reinstatement value, also known as the new replacement value, is the point at which the insured regains the position he had before the incident.

3. Does Fire Insurance cover the insured for a long period of time?

Insureds are covered for 12 months under the Fire Insurance Policy.

4. If the insured cancels the Fire Insurance Policy and pays the premium back, can the premium be refunded?

Fire Insurance Policy can be canceled at any time with a pro-rated refund of premiums.

5. What can I do to increase the coverage under Fire Insurance Policy?

It is possible to increase coverage by purchasing insurance add-ons.

6. When purchasing Fire Insurance Policy, can partial selections of assets be made?

It is not possible to select parts of the assets. The entire value of plant and machinery, FFF, and stock is covered by the Fire Insurance Policy based on the risk assumptions.

7. What is the time frame for getting theft coverage?

When theft occurs, the insurer will provide coverage within 7 days of the event.

8. What are the options for increasing the inbuilt sum insured limit?

The inbuilt covers do not currently offer the option to increase the sum insured limit, according to IRDAI guidelines.

9. Does the plan include a provision for excluding inbuilt perils so that the price can be reduced?

There is no provision in the Fire Insurance Policy to exclude inbuilt perils.

10. Can Fire Insurance Policy be purchased by any commercial enterprise?

Risks associated with hotels, offices, shops, manufacturing and industrial plants, utilities kept outside the compound, storage risks, and owners of tanks outside the compound.

11. What is the premium for Fire Insurance Policy and how is it calculated?

Insurance premiums are based on the following factors: Insured sum, insured properties, plant & machinery, buildings, stocks, etc.

12. When does the insured have the option of changing the Fire Insurance Policy?

The coverage part of your policy can be changed. Adding or removing any add-on will result in an increase or decrease in the premium amount. This only takes effect once the insurer accepts it and you have paid the extra amount.

Read more about FLOP Policy