What is a CAR Policy?

A Contractor’s All Risk (CAR) Policy, also known as a Construction All Risk Policy, is an insurance policy that provides comprehensive coverage for construction projects. It covers various risks that contractors and builders may face during the construction process. A Contractor’s All Risk Policy in construction is designed to protect contractors and builders from financial losses that may arise due to unforeseen events during the construction process. As we will find out in subsequent sections of this blog, this policy is particularly important for construction projects that involve a high degree of risk, such as those that involve working at heights, working with heavy machinery, or working in hazardous environments.

Let’s start with the basics then!

Contractors All Risk Policy in Construction

A Contractor’s All Risk Policy is a type of insurance policy that provides coverage for construction projects against loss or damage. It is designed to protect contractors and builders from financial losses that may arise due to unforeseen events during the course of construction. The Contractors All Risk policy is usually taken out by a commercial contractor or builder, but it can also be taken out by the owner of the project. The policy can be tailored to meet the specific needs of the project and can be extended to cover additional risks such as terrorism, earthquakes, and floods.

The policy period usually begins from the start of the construction work and ends when the project is completed. The premium for the policy is based on factors such as the estimated value of the project, the type of construction, and the level of risk involved.

Coverage Provided in a Contractors All Risk Policy in Construction

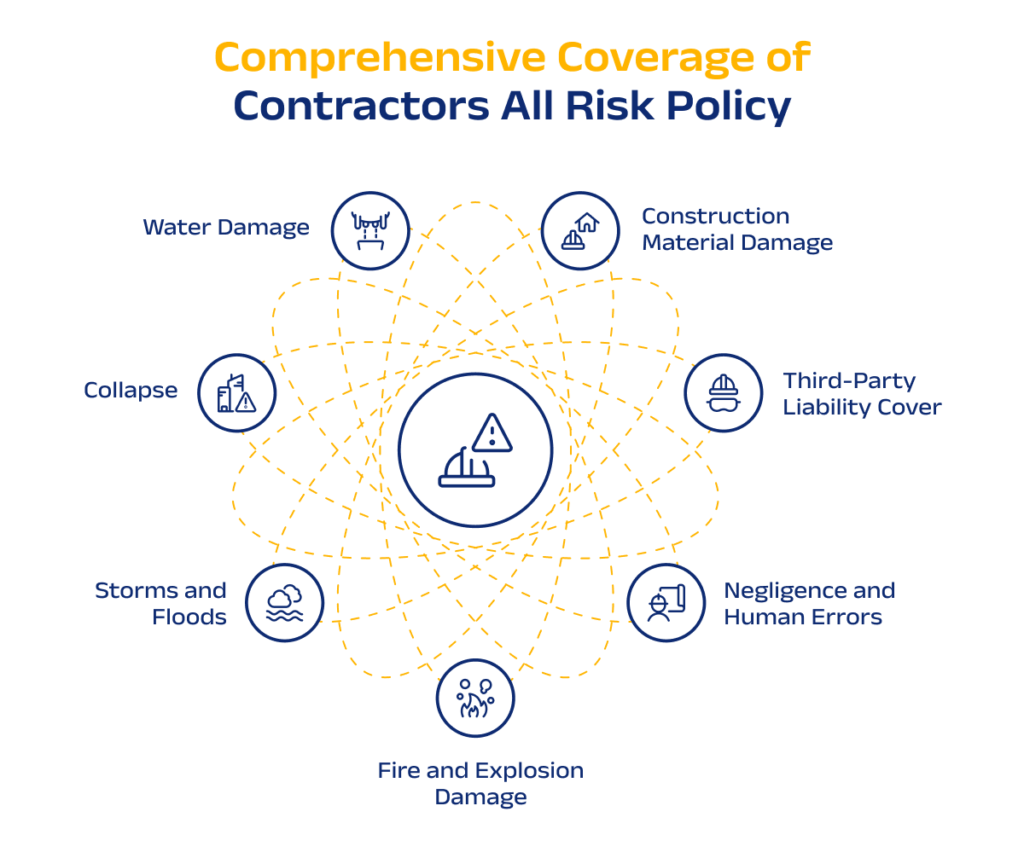

A Contractor’s All Risk policy provides comprehensive coverage for construction projects. It covers loss or damage to the property under construction, as well as third-party liability arising from the project. This section will discuss the scope of coverage provided by a typical Contractors All Risk Policy.

1. Construction Material Damage: A Contractors All Risk Policy in construction provides coverage for loss or damage to the property under construction. This includes damage to the building or structure, as well as any materials or equipment on site. The policy compensates losses due to a wide range of covered perils, including fire, theft, natural disasters, and accidental damage. It may also cover the costs of demolition, removal of damaged materials, and debris cleanup. In addition, a Contractors All Risk policy can also cover damage to existing structures that may occur during the construction process. This is known as “existing property cover.”

2. Third-Party Liability Cover: A Contractors All Risk policy also provides coverage for third-party liability arising from the construction project. This includes bodily injury or property damage that may occur to third parties, such as passersby or neighbouring properties. The policy also covers legal expenses and compensation that may be payable to third parties.

3. Negligence and Human Errors: A Contractors All Risk policy in construction may include coverage for claims related to professional negligence or errors in design, planning, or project management. This insurance often covers losses resulting from faulty workmanship, design errors, or defective materials as well. If a construction project suffers damage due to errors in construction or design, the policy may provide compensation for rectification and repair costs.

4. Fire, Explosion, Lightning, and Aircraft Damage: A Contractor All Risk policy provides coverage for damages caused by accidental fires on the construction site. Additionally, the policy extends coverage to damages resulting from explosions, whether due to accidental events or unforeseen circumstances. Lightning damage is also covered, offering compensation for losses caused by lightning strikes during the construction period. Moreover, in the event of damage caused by aircraft, such as crashes or debris, a Contractors All Risk policy steps in to provide the necessary financial support for repairs or replacements.

5. Storms, Floods, Cyclones, Earthquakes, and Allied Perils: This policy includes protection against storms, floods, cyclones, earthquakes, and allied perils, ensuring financial support for damages resulting from these events. Storms, including windstorms and hailstorms, can cause significant damage to construction sites, and a Contractors All Risk Policy covers the cost of repairs or replacements. Floods, which may result from heavy rainfall or other water-related incidents, are also addressed in the policy, providing coverage for losses incurred due to water damage. Similarly, cyclones and earthquakes, which pose substantial risks to construction projects, are covered, offering a safety net for expenses related to structural damage or other construction-related losses.

6. Collapse: In the unfortunate event of a partial or total collapse of the insured structure during the construction phase, the Contractors All Risk policy provides financial protection to the insured. It covers the costs associated with the necessary repairs or reconstruction of the affected structures. This aspect of the policy is instrumental in mitigating the substantial financial burden that may arise due to such unforeseen circumstances jeopardizing the stability of the construction site.

7. Water damage: A Contractors All Risk Policy includes protection for losses incurred due to various water-related incidents, such as floods, heavy rainfall, water seepage, or accidental discharge. The policy covers repair or replacement costs for damages to the construction site, materials, and equipment caused by water-related events.

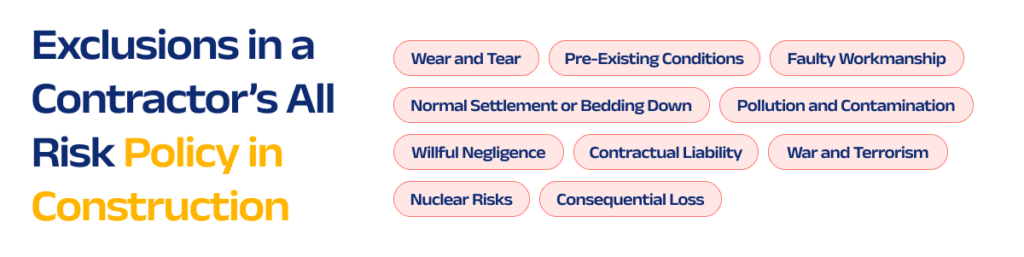

Exclusions in a Contractor’s All Risk Policy in Construction

While a Contractors All Risk Policy in construction provides comprehensive coverage, certain exclusions are not covered by the policy. Some of the common exclusions include:

· Wear and Tear: Damage resulting from normal wear and tear, gradual deterioration, or depreciation of materials and equipment over time.

· Pre-Existing Conditions: Any damages or defects that existed before the insurance policy came into effect may be excluded.

· Faulty Workmanship: Excludes coverage for losses arising from faulty workmanship that occurred before or during the construction phase.

· Willful Negligence: Damages caused intentionally or due to willful negligence on the part of the insured party may be excluded.

· Contractual Liability: Excludes liabilities assumed by the insured under contract unless the liability would have existed in the absence of the contract.

· Nuclear Risks: Damage caused by nuclear reactions, radiation, or radioactive contamination is typically excluded.

· War and Terrorism: Losses resulting from war, acts of terrorism, or civil unrest are often excluded.

· Normal Settlement or Bedding Down: Excludes damage caused by the normal settlement or bedding down of new structures.

· Consequential Loss: Losses or damages resulting from business interruption, loss of profit, or other consequential losses may be excluded.

· Pollution and Contamination: Damage caused by pollution or contamination may be excluded from coverage.

It is crucial for policyholders to carefully review the terms and conditions of their specific Contractors All Risk policy to understand the exclusions that apply. Additionally, discussing these exclusions with an insurance advisor or broker can help ensure a clear understanding of the limitations of coverage and allow for any necessary adjustments to the policy or risk management strategies.

Claim Process in a Contractor All Risk Policy in Construction

· Notification of Loss

In the event of a loss, the policyholder must notify the insurer immediately. The notification should include details of the incident, the date and time of the loss, and the estimated cost of the damage. The policyholder should also provide their policy number and contact details.

· Documentation Required

The insurer will require documentation to support the claim. This may include photographs of the damage, invoices for repairs, and any other relevant documents. The policyholder should ensure that they keep all receipts and invoices related to the loss.

· Assessment and Settlement

Once the insurer has received the notification of loss and all relevant documentation, they will assess the claim. The insurer may appoint a loss adjuster to investigate the claim and assess the extent of the damage. The loss adjuster will provide a report to the insurer, which will be used to determine the settlement amount.

The insurer will then settle the claim in accordance with the policy terms and conditions. The settlement amount may be paid in cash or kind, depending on the policy terms. The policyholder should ensure that they have read and understood the policy terms and conditions to avoid any misunderstandings during the claim process.

Factors affecting Premium Calculation in a CAR Policy in Construction

Contractor’s all risk policy premiums are calculated based on several factors. These factors include:

1. Contract Value

The contract value is the total sum of money agreed upon between the contractor and the client for the project. The higher the contract value, the higher the premium will be.

2. Nature of the Project

The nature of the construction project is also taken into consideration when calculating the premium. Projects that involve higher risks such as demolition, excavation, and tunneling will have a higher premium compared to less risky projects.

3. Duration of the Project

The duration of the project is another factor that affects the premium. Longer projects will have higher premiums compared to shorter ones.

4. Location of the Project

The location of the project is also taken into consideration when calculating the premium. Projects located in areas with higher risks such as earthquake-prone zones or areas with a high crime rate will have a higher premium.

5. Experience of the Contractor

The experience of the contractor is also a factor that affects the premium. Contractors with a good track record and experience in handling similar projects will have a lower premium compared to those who are inexperienced.

Frequently Asked Questions

1. What is the full form of CAR Policy?

The full form of CAR Policy is Contractors’ All Risks insurance. This policy covers property damage and third-party injury or claims during construction. CAR insurance protects both contractors and project owners from unexpected site-related losses and liabilities.

2. How is the sum insured determined for a Contractor’s All Risk insurance policy?

The sum insured for a Contractor’s All Risk insurance policy is determined based on the estimated cost of the construction project. This includes the cost of materials, labor, and other expenses related to the construction. The sum insured should be sufficient to cover the total cost of the project in case of any loss or damage.

3. In what ways does the Extend Maintenance Cover benefit the policyholder in a CAR Policy?

Extended maintenance cover provides additional protection to the policyholder after the construction project is completed. It covers any defects or damage that may arise during the maintenance period. This ensures that the policyholder is protected against any unforeseen expenses that may arise due to maintenance issues.

4. How does the CAR policy coverage differ from other forms of construction insurance?

The CAR Policy coverage is broader than other forms of construction insurance. It covers loss or damage to the construction project during the period of construction, including third-party liability. Other forms of construction insurance may not provide such comprehensive coverage.