In the ever-evolving landscape of construction projects, risk mitigation stands as a paramount concern for all stakeholders involved. Among the array of safeguards available, Erection All Risk (EAR) Insurance emerges as a beacon of financial protection and peace of mind. From colossal skyscrapers to intricate industrial facilities, the scope and complexity of modern construction ventures necessitate a comprehensive shield against unforeseen perils.

This article looks into the intricate realm of Erection All Risk insurance. Join us as we unravel the layers of protection offered by EAR insurance, unravel its intricacies, and empower your projects to rise confidently amidst the uncertainties of the construction landscape.

To start with, let’s turn our attention to the basics.

What is Erection All Risk Insurance Policy?

In an Erection All Risk (EAR) policy, you are protected when installing machinery or equipment in your factory or office. The policy covers any losses or damages that occur during installation. If anything goes wrong, you will be reimbursed financially, which could slow down the installation and increase costs.

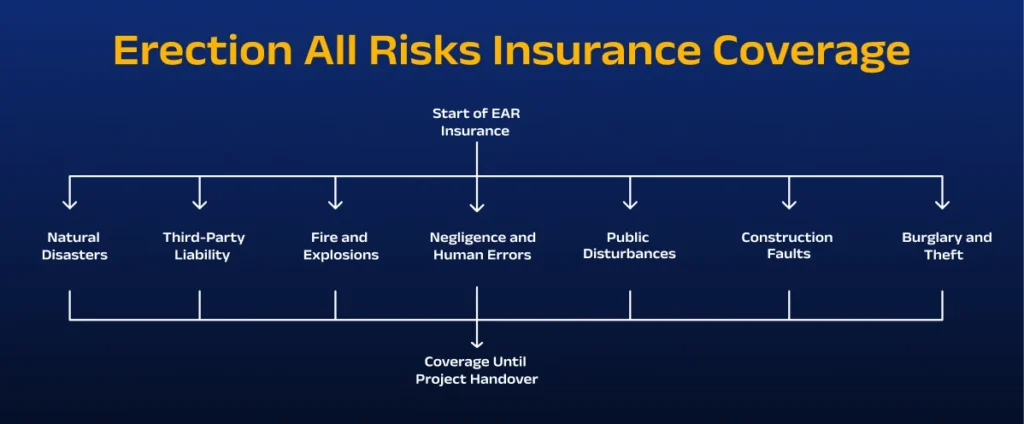

EAR insurance coverage begins the moment materials are unloaded at the construction site and continues until the client has received the completed project.

What is the Misconception About the Erection All Risk Insurance?

Plants and machinery are often misunderstood as being insured only after they have been installed and tested. However, EAR policies cover you while equipment is being installed, whether it’s a single machine or a large power plant.

What are Some of the Salient Features of Erection All Risk Policy?

· The policy covers heavy machinery and plant at the insured site during storage, erection, and testing, in addition to providing comprehensive coverage for the erection of projects.

· The Coverage is provided throughout the project lifecycle rather than on a yearly basis.

· There are a variety of features that can be added by customers.

Who are Eligible for EAR insurance Policy?

This policy can be taken out jointly or individually by contractors and employers. The following parties may be covered:

· General & subcontractors

· Manufacturers and suppliers of equipment

· Purchaser or owner of the equipment

Erection All Risk Policy (EAR): Why Do You Need It?

An Erection All Risk Policy is useful if you work in the construction industry. It’s a comprehensive insurance policy that protects you when things go wrong while you’re installing, testing, or starting up equipment. With BimaKavach, you’ll be able to get personalized quotes from the best insurance companies at an affordable price.

What is Included in the Erection All Risk Insurance Policy?

EAR (Erection All Risks) insurance coverage starts when the first delivery reaches the project site. Here are some of the things covered by this insurance. It lasts until the testing is completed or until the project is handed over to the main employer.

Storms, floods, cyclones, earthquakes, and allied perils – In the event of any loss or damage caused by these covered perils during the installation period, it is covered. Storms, overflowing rivers, heavy rain, other flood-related events, cyclonic events, tremors, other earthquake-related factors, and other related perils can damage the construction site, materials, equipment, or structures.

Third-Party Liability – It provides legal liability coverage for the insured in the event of accidental damage or loss to a third party’s property because of his or her erection work. The insurance also covers the legal liability for injury to a third party.

Damage from explosion, fire, lightning, and aircraft damage – When these specific perils occur during construction or installation, this cover provides coverage for losses or damages. A fire or explosion caused by a fire or explosion can damage the construction site, materials, equipment, and structures. A construction site can suffer damage or destruction due to gas leaks, chemical reactions, fires caused by lightning, electrical surges, and collisions with aircraft.

Negligence and Human Errors – A common feature of EAR insurance is that it covers losses resulting from negligence and errors in planning, designing, or supervising the erection process. Liability claims arising from negligence or human error that result in property or personal injury to third parties are also covered by an EAR insurance policy.

Riots & Strike– During riots, demonstrations, protests, or other forms of public disturbances, this coverage covers damage to the construction site, materials, equipment, or structures. In addition, it covers damage caused by strikes, lockouts, labor disputes, or other events related to the construction project.

Building Erection Faults-During the construction of the project, this coverage covers issues related to construction defects, workmanship errors, and defective installation. Insufficient materials, inadequate workmanship, or faulty design results in structural failures or defects because of improper construction methods, improper construction methods, or inadequate materials. There may also be errors in measurements, assembly, installation, or other issues that lead to defects.

Burglary & theft – This coverage addresses the risk of theft or burglary-related incidents that may occur at the construction site or involve the insured property. This is applicable to thefts involving construction equipment, tools, machinery, and other valuables. A Burglary Policy also covers losses or damages resulting from unauthorized entry into locked garages or storage areas, as well as forced entry into locked premises.

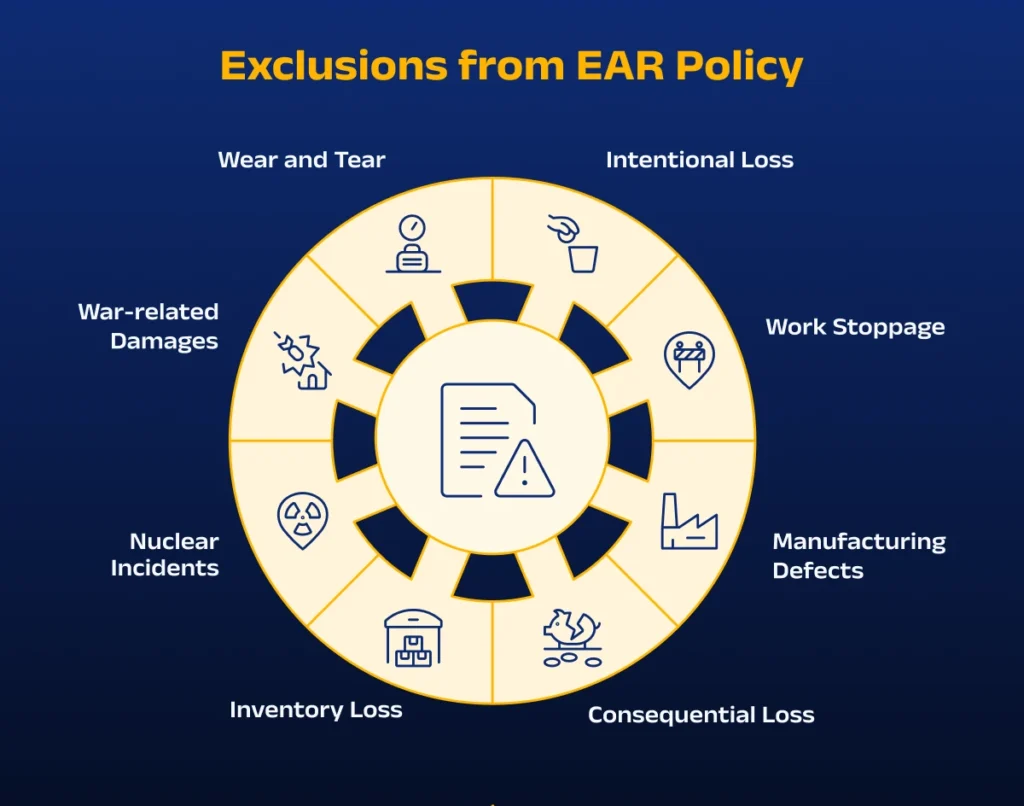

What is Not Included in EAR Policy?

· Intentional or negligent loss or damage

· Work stoppage

· A defect in the manufacturing process

· Loss of consequential nature

· Loss of inventory

· A nuclear reaction, radioactive contamination, or nuclear radiation can cause loss or damage.

· War-related losses or damages

· Normal wear and tear and gradual deterioration losses

What are the Add-on Covers in EAR Insurance Policy?

Your insurance coverage can be extended by choosing from the available add-ons below.

· Liability for both parties

· The cost of clearing and removing debris

· Third-party liability

· Express freight

· Additional customs duty

· Airfreight

· Escalation

· Property damage to the surrounding area

· Maintenance Cover

· Overtime and holiday charges

Example 1 – A claim for a machinery collapse during installation

During the process of installing a large industrial machine at a factory, a construction company experiences an unfortunate incident where the machinery collapses, causing damage to the surrounding area. An EAR Insurance policy would cover the damage caused to adjacent buildings, infrastructure, and any other assets that were damaged by the collapse of the machinery if the contractor has obtained it.

If the contractor has acquired an EAR Insurance Policy to safeguard their project against multiple risks, including third-party liability, said the policy would extend coverage for the contractor’s liability. This encompasses any harm inflicted upon nearby property like adjacent buildings, infrastructure, or other affected assets resulting from machinery collapse. Moreover, it would also offer protection for injuries suffered by subcontractor workers. Additionally, potential legal liabilities stemming from bodily injury would be covered under this policy as well.

Example 2 – A claim for an electrical system connection that is faulty

Suppose a contractor installs a new electrical system in a commercial building as part of a construction project. As a result of a faulty connection during installation, a fire breaks out, damaging the building and the electrical equipment.

EAR Insurance covers damage caused by fire to both the building and the electrical equipment being installed if the contractor has obtained it to protect its project from a variety of risks, including fire damage. In addition to repairing or replacing the building’s structure, electrical wiring, panels, switches, and other related components, it also covers the cost of replacing or repairing the damage.

The footnote:

Throughout the exploration of EAR insurance above, we have gained a profound understanding of its significance, coverage inclusions, and limitations. In a world where construction projects and infrastructure development shape our landscapes, the need for comprehensive insurance coverage has never been more crucial. Erection All Risk Insurance (EAR) stands as a steadfast pillar, providing a comprehensive safety net for both project owners and contractors alike.

By harnessing the power of EAR insurance and understanding both its inclusions and exclusions, project owners and contractors can foster an environment of collaboration, innovation, and progress, as they transform visions into reality. As the world continues to evolve, and new challenges emerge, EAR insurance stands strong as a shield of protection, empowering construction stakeholders to forge ahead with confidence and assurance.

Have You Asked Yourself the Following Questions –

1. How do EAR and CAR Policies differ from one another?

A CAR Policy protects construction companies and contractors against all risks and is most widely used for the movement of debris and concrete building activity, which makes it a better fit for civil construction projects, such as buildings, bridges, roads, and ports.

EAR coverage, on the other hand, is taken while installing machinery and equipment. It is more suitable for engineering facilities and other construction projects that include erections and installations. Power plants, gas processing facilities, and other facilities are covered by EAR insurance policies, for example.

2. Is the EAR Policy available to anyone?

All parties involved in any type of construction can be insured by a joint policy purchased by the contractor and employer.

· Contractors in general

· Subcontractors

· Equipment suppliers and manufacturers

· Purchaser or proprietor

3. How long does the extended maintenance period in the EAR Policy last?

Under an EAR Policy, an extended maintenance period extends the duration of coverage beyond the scheduled completion date for a specified period, typically several months to a year. The insured contractor must complete outstanding work and remedy defects according to the contract provisions during this period.

4. Is it important to get an Erection All Risk Insurance Policy?

In India, Erection All Risk (EAR) insurance is not specifically required by law; however, taking out an EAR Policy is a good idea if you’re involved in construction. There are several risks involved in this type of project, and an EAR Policy can protect you financially in the event of a loss. It is a small investment that can provide you with peace of mind, along with financial protection in the event of a loss.

5. How long does the Erection All Risk Policy give you to submit claims?

Generally, it is best to submit your claim paperwork as soon as you receive it. Each insurer sets a deadline for submitting claims, so it is often advisable to submit all relevant documents as soon as possible.

6. Is there a documentation requirement for filing a claim under the Erection All-risk Insurance Policy?

When filing an EAR claim, some common documents are typically required.

· Detailed Request for Quotation

· Details related to Principal, Contractor, and Subcontractor.

· The estimated cost of the project

· The start and end date of the project

· Details related to Testing for EAR projects.

· Equipment details for EAR projects

· Sum Insured breakdown for different scopes of work.

· Location details of the risk

· Where there is more than one location, the coordinates and names of all locations should be provided

· A complete/detailed scope of works or a copy of the contract.

· Details of the wet work if any

7. What types of people can be insured under the EAR Policy?

A general contractor, subcontractor, equipment supplier, manufacturer, and buyer can be insured under this policy. Employers, as well as contractors, can be insured individually or jointly.

8. How is the premium computed for the Erection All Risk policy?

An insurance company examines several aspects while calculating risks and quoting the premium for the Erection All Risk Insurance Policy. These criteria include the scope, location, cost, and time frame for the construction work.

9. Can the Erection All Risks Insurance Policy cover financial losses caused by delays in the completion of the project?

Yes. Most Erection All Risk Policies provide coverage for financial losses during the erection process, including delays in the construction schedule.

10. What do AOG perils mean?

In insurance, “Act of God” (AOG) is a term used to describe perils or events that are beyond human control and are not caused by human action or negligence. These perils are typically covered under insurance policies to provide protection against losses. Acts of God’s perils can include a wide range of events, such as earthquakes, hurricanes, floods, lightning strikes, volcanic eruptions, tsunamis, fires caused by natural factors, and other catastrophic events.

11. How is the premium calculated for erection all risk?

Here is how premium is calculated:

Sum Insured – The higher the sum insured, the higher the premium; and vice versa.

Project Duration – A longer installation period will result in a higher premium.

Type of Project: Projects with higher risks, such as large-scale infrastructure developments or projects involving environmental and location risk, may attract higher premium.

Testing Period – As soon as the new machinery is installed, it is tested before being handed over to its owners. This period is used to calculate the premium.

Insureds seek voluntary access – A voluntary excess option, if availed as part of the policy, may result in a reduction in premiums.

12- What is the claim procedure of EAR Policy?

The insured shall –

Provide all information and documentation as requested by the company.

Inform the broker, he will handhold and guide you throughout the claim settlement process.

Notify the police in case of theft or burglary losses or damages at the construction site.

Cooperate with the surveyor of the company to make him inspect the affected parts.